Canada's banking regulator proposes to purge higher-risk borrowers from the mortgage market.

OSFI says it's worried about banks being "exposed to heightened risks" from record indebtedness, potential recession and multi-decade highs in interest rates.

Encouraging lower indebtedness "reduces the probability of borrower default by making ongoing debt payments more manageable and limits lenders' potential losses in case of borrower default," OSFI explained in its announcement Thursday.

In my exclusive Globe interview with OSFI head Peter Routledge on Wednesday, he told me, “What we’re trying to construct is an underwriting system that ensures that folks who get into the housing market through a mortgage can service that mortgage through unexpected events—loss of a job, divorce, sudden increase in interest rates.”

"This is a two-part consultation," OSFI says. "The initial phase opens on January 12, 2023 and ends on April 14, 2023. Feedback from this consultation will inform proposed revisions to Guideline B-20, which will be issued in the second phase—in draft form—for public consultation at a future date."

The regulator has proposed three types of mortgage underwriting restrictions for public comment: loan-to-income limits, debt ratio limits and stress test tweaks. We'll run down each of them here, with comments from Mr. Routledge:

#1 - New loan-to-income (LTI) and debt-to-income (DTI) restrictions

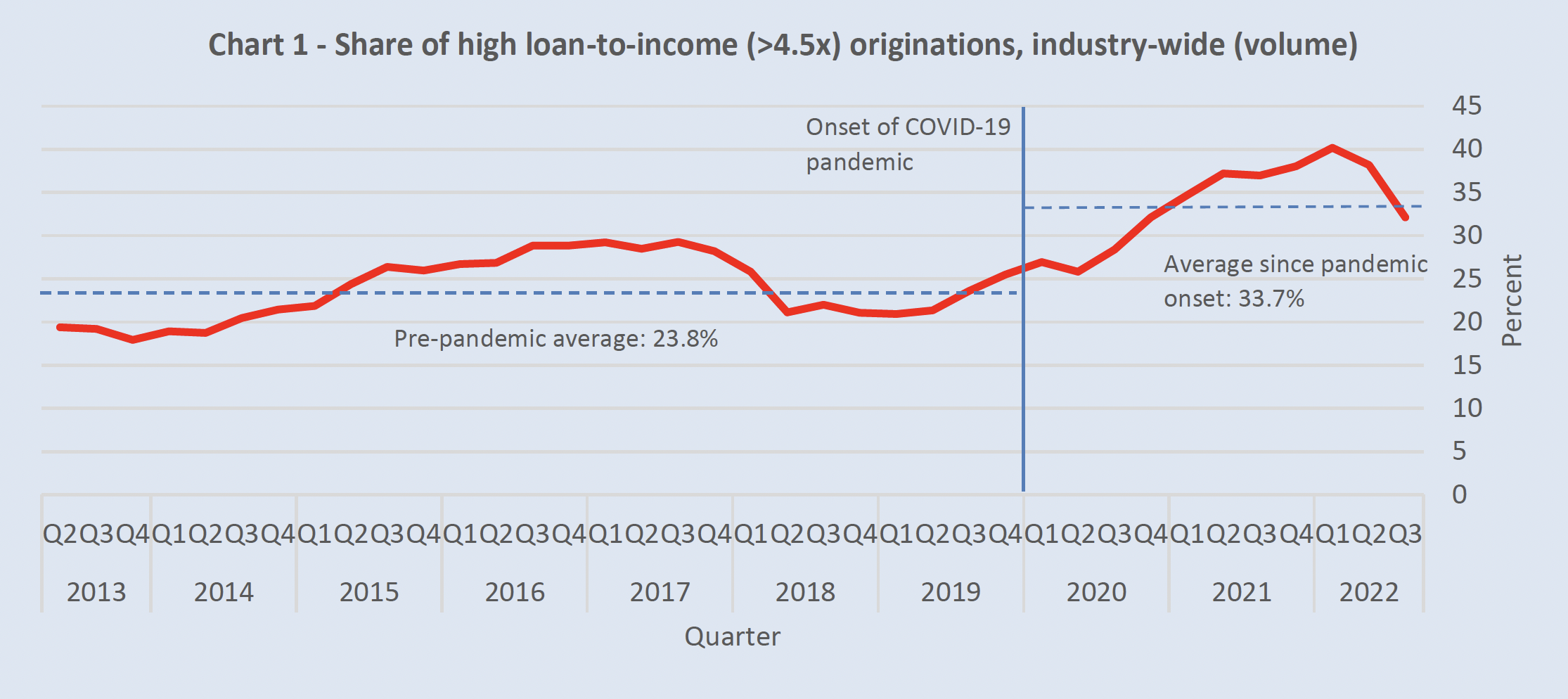

OSFI proposes to adopt one of former-CMHC chief Evan Siddall's favourite prudential restrictions, an overall limit on mortgage size based on annual income. Specifically, the regulator is asking whether banks should be restricted from granting more than, say, 25% of their mortgages (by dollar volume) to borrowers with a loan-to-income (LTI) ratio of 450% or more.

OSFI calculates LTI as the mortgage amount divided by the borrower’s qualifying annual income.

During the COVID lockdowns, “we did see a boom in lending,” Routledge said. The percent of mortgagors who have high LTI ratios (450%+) went from around 14% to 26%. “So that’s pretty significant risk concentration and that happened even with the mortgage stress test in place,” he explained.

An LTI ratio “is not something that’s specific to every borrower,” Routledge added. “In the future, we’re not proposing that you walk into your bank branch and they say, ‘Oh, your loan is more than 450% of income so no thank you.' We’re not going to intervene in that way.”

"What we’re talking about is that over a given time period, not more than X% of mortgages breach that 450% of income."

OSFI also said it is evaluating whether to restrict total indebtedness as a multiple, or percentage, of borrower income. That would be even more restrictive.

#2 - New debt ratio limits

Unlike insured mortgages, debt ratio limits on uninsured mortgages are not specifically regulated. That could change.

Routledge says OSFI is essentially asking the industry if a hard cap on uninsured debt ratios is a “viable way of adding resilience to the system.”

Specifically, OSFI is considering:

- Tweaking the formulas and definitions for gross debt service (GDS) and total debt service (TDS) —perhaps adopting those that currently exist for insured mortgages

- Graduated or tiered GDS and TDS limits

- An explicit amortization limit to be used in GDS and TDS calculations.

- Potential new capital restrictions for high GDS/TDS mortgages.

"Today, within bank policies they do allow exceptions," Routledge explained. There is no hard cap on debt service in the uninsured realm. “What we’re going to ask our institutions is, does that still work to contain risk concentrations? And if it doesn’t, what could we do to make it better? And we’ll see what the answers are.”

#3 - New interest rate stress tests

Floating-rate and short-term mortgages "can carry heightened payment and renewal risk," OSFI says. It suggests that it may be appropriate to strengthen the affordability test on such mortgages while making longer fixed terms, which "pose less risk," relatively easier to qualify for.

There was a period of "three to seven months" where the mortgage stress test for variable rates was lower than for fixed rates, Routledge said. This led a very small percentage of borrowers to choose riskier terms in order to qualify for a mortgage.

“That does concern us," he said. "We, generally speaking, would prefer not to have a mortgage interest rate stress test favour one particular product over another. In the difficulty of constructing a simple test that people can understand, you can’t get that perfection. You can’t get that level of precision.”

“In our consultations with industry, we came to understand that that gap was not a material factor in determining whether someone went with variable or fixed. I’m not saying for everyone always that was the case, but we looked very closely at this and our regulated constituents told us, “no, it was never really a factor over those three to seven months.”

Routledge called it “unlikely” that OSFI would amend the stress test to address this specific situation, given the regulator “didn’t see it as materially affecting the market overall.”

Last but not least, OSFI has also proposed applying the minimum qualifying rate to non-mortgage debt, when calculating a borrower's TDS ratio. Today, lenders still use the actual interest rate to calculate non-mortgage payments for certain non-revolving debts.

Fixing what ain't broken (yet?)

“Debt serviceability is among the strongest it’s ever been," Routledge says. “99.86% of Canadians are current on their mortgages, and that’s the best it’s been in terms of our recorded history."

“We’re quite confident" banks could withstand a major recession and housing crash, he said. "We do detailed stress testing on a bilateral basis with the institutions we regulate and we have a lot of resilience built into the capital and liquidity of those institutions to withstand and absorb a major shock..."

“Canadians are absorbing higher debt service costs and I think the mortgage stress test…has contributed mightily to that good outcome.”

Right, so what's the problem again?

Well, “The nature of risk is that there’s the risk you see, and you adapt to those as best you can," he explains. "And then there are the risks over the horizon you can’t see but you know they’re going to come up over the horizon at some point.”

“Our mantra internally is, we’ll act early, accept some of the criticism that comes from acting early, in order to minimize the risks of acting too late. Acting too late often gets you higher costs than you otherwise would like in the financial system.”

OSFI's impact on home prices and creating procyclicality to Canada's downturn are “legitimate" and "we concern ourselves with them,” Routledge says. But it won't stop the regulator from acting.

Shuffling riskier borrowers to non-federally regulated lenders

Routledge didn't accept the premise that banishing higher-indebted borrowers to non-prime lenders would potentially come back to bite us.

Over the last dozen years or so, “we haven’t really seen the market share shift out of” the federally regulated mortgage market to the non-federally regulated market," he said.

Market share of non-regulated lenders, like mortgage investment corporations, is “a very small percent,” albeit their “growth has been rapid" and "we’re watchful of that,” he said.

Routledge added that OSFI is respectful of Canada being a free-market economy and that borrowers deserve the right to access more flexible less-regulated lenders. “We don’t propose to interfere with that. We’re just trying to create structure and resilience within the system we regulate.”

The regulator's intention...

“We know how important mortgages are to Canadians," says Routledge. "We know the manner in which we try and promote a stable resilient mortgage underwriting system affects everyday Canadians every day.”

"We’ve thrown out some ideas we’re considering," he says. "We’re opening up the consultation early. We want ideas. We want constructive critiques. We want to hear from players in the system."

"Out of that will emerge an adjustment, or not, to how we will continue to regulate and supervise the residential mortgage credit system for federally regulated financial institutions, in a manner that sustains resilience…”

“We think of what we’re doing here today as not to address concerns that may have come out of stress tests.”

“What we’re doing today is to ensure that residential mortgage credit underwriting quality remains high, that unforeseen risk concentrations over the horizon, we’re are least preparing for early.”

OSFI wouldn't say when the final guideline could be announced, but my best guess is somewhere near the third quarter. That'll give the housing market more time to digest high rates and rising unemployment.